Gross income is calculated by subtracting the cost of goods sold from a company’s revenue for a given period. Therefore, when COGS is lower (as it is under FIFO), a company will report a higher gross income statement. Higher inflation rates will increase the difference between the FIFO and LIFO methods since prices will change more rapidly. If inflation is high, products purchased in July may be significantly cheaper than products purchased in September. Under FIFO, we assume all of the July products are sold first, leaving a high-value remaining inventory. Under LIFO, September products are sold first even if July products are left over, leaving the remaining at a low value.

Why should you not choose LIFO?

In total, the cost of the widgets under the LIFO method is $1,200, or five at $200 and two at $100. On the other hand, manufacturers create products and must account for the material, labor, and overhead costs incurred to produce the units and store them in inventory for resale. LIFO second home tax tips is more difficult to account for because the newest units purchased are constantly changing. However, if there are five purchases, the first units sold are at $58.25. Using FIFO simplifies the accounting process because the oldest items in inventory are assumed to be sold first.

Track and manage time

As such, FIFO is a generally accepted accounting principle in almost all jurisdictions, whereas LIFO accounting is only accepted in some. It’s important to check industry standards in your jurisdiction to ensure your valuation method meets regulatory compliance. The type of inventory that a business holds can influence its choice of FIFO or LIFO. For example, businesses with a beginning inventory of perishable goods will usually choose FIFO, since it’s in their best interest to sell older products before they expire. Using the appropriate inventory valuation system can help track real inventory management practices.

Understanding the inventory formula

This is because older inventory was often purchased at a lower price and the market may have changed since the early orders. The First In, First Out FIFO method is a standard accounting practice that assumes that assets are sold in the same order they’re bought. All companies are required to use the FIFO method to account for inventory in some jurisdictions but FIFO is a popular standard due to its ease and transparency even where it isn’t mandated.

With Deborah Gemborowski, CPA, P.C., you can focus on running your business, while we keep your accounting in line. Inventory is assigned costs as items are prepared for sale and based on the order in which the product was used. Every business is different, and good software lets you customize it to fit your needs. Whether you’re dealing with perishable items or long-lasting goods, you can set it up to manage your inventory in a way that works best for you.

If you manufacture products that can expire, such as food or pharmaceuticals, FIFO might be your best option. In a similar vein, it’s worth mentioning FEFO (First Expired, First Out), which is very similar to FIFO, but specifically works based on expiry dates of goods. If your products don’t spoil (think hardware or furniture), LIFO may be better. LIFO matches the most recent costs with your current sales, which is great if and when prices go up. With this method, your product’s final cost is based on the price you paid for the oldest inventory. FIFO inventory valuation is great for businesses that deal with perishable goods or products that can quickly lose value, such as food products or tech gadgets.

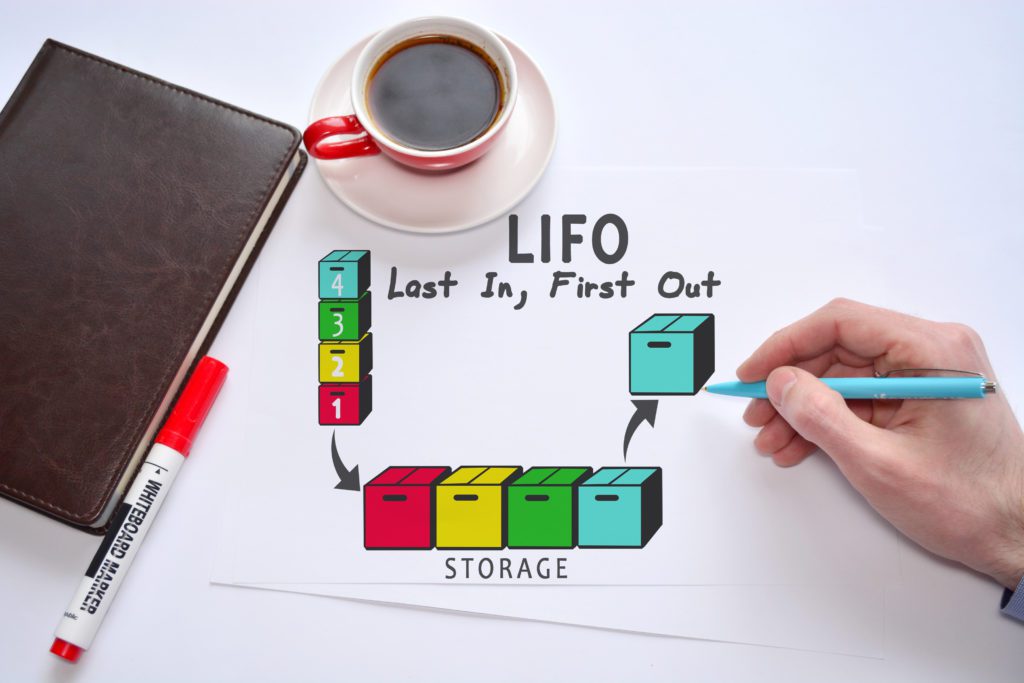

FIFO means “First In, First Out.” It’s an asset management and valuation method in which older inventory is moved out before new inventory comes in. In general, FIFO is a safer bet than LIFO because there aren’t restrictions from the GAAP or IFRS. However, your business may benefit from LIFO inventory if it’s allowed. To know which method is best suited for your business, you need to look at the way your inventory costs are changing. It’s a method of inventory management and valuation in which goods produced or acquired first are sold, used, or disposed of first. Let’s say you own a craft supply store specializing in materials for beading.

- This can lead to a substantial tax burden, which might strain cash flow, especially for businesses with tight margins.

- Try FreshBooks free to discover how streamlining your inventory process can help you grow your small business today.

- FIFO and LIFO are both approved by GAAP – the Generally Accepted Accounting Principles, which is used in the USA.

- We’ll calculate the cost of goods sold balance and ending inventory, starting with the FIFO method.

FIFO and LIFO are the two most common inventory valuation methods used by public companies, per U.S. Using FIFO does not necessarily mean that all the oldest inventory has been sold first—rather, it’s used as an assumption for calculation purposes. Learn more about what FIFO is and how it’s used to decide which inventory valuation methods are the right fit for your business. Assuming that prices are rising, this means that inventory levels are going to be highest as the most recent goods (often the most expensive) are being kept in inventory. This also means that the earliest goods (often the least expensive) are reported under the cost of goods sold.

For investors, inventory can be one of the most important items to analyze because it can provide insight into what’s happening with a company’s core business. The valuation method that a company uses can vary across different industries. Below are some of the differences between LIFO and FIFO when considering the valuation of inventory and its impact on COGS and profits. FIFO is generally accepted as the more accurate inventory valuation system.

FIFO and LIFO have different impacts on inventory management and inventory valuation. In most cases, businesses will choose an inventory valuation method that matches their real inventory flow. Thus, businesses that choose FIFO will try to sell their oldest products first. FIFO and LIFO are common inventory valuation methods used to understand the value of unsold stock in the balance sheet and inform key financial metrics like the cost of goods sold.

As with FIFO, if the price to acquire the products in inventory fluctuates during the specific time period you are calculating COGS for, that has to be taken into account. Companies with perishable goods or items heavily subject to obsolescence are more likely to use LIFO. Logistically, that grocery store is more likely to try to sell slightly older bananas as opposed to the most recently delivered. Should the company sell the most recent perishable good it receives, the oldest inventory items will likely go bad. Despite increasing production costs, Company A retains a consistent sales price of $400 per vacuum. They sell 200 vacuums in the first quarter, generating a revenue of $80,000.